The insurance industry is a vital part of the global economy. It protects individuals and businesses against financial losses resulting from unexpected events such as accidents, illnesses, and natural disasters. The industry constantly evolves due to technological advancements, changing customer expectations, and regulatory pressures. Insurers use digital technologies to provide customers fast, convenient, personalized service.

The industry is facing several challenges, including the need to keep up with and manage technology and innovation, attract and retain top talent, remain competitive with new disruptors in the industry, and adapt to changing customer expectations.

The future of the insurance industry is likely to be shaped by several key disruptors. These include technology-driven changes such as artificial intelligence (AI), blockchain, the Internet of Things (IoT), and changing customer expectations. Insurance companies will need to articulate their strategy and adjust their operating models accordingly to stay ahead of the curve.

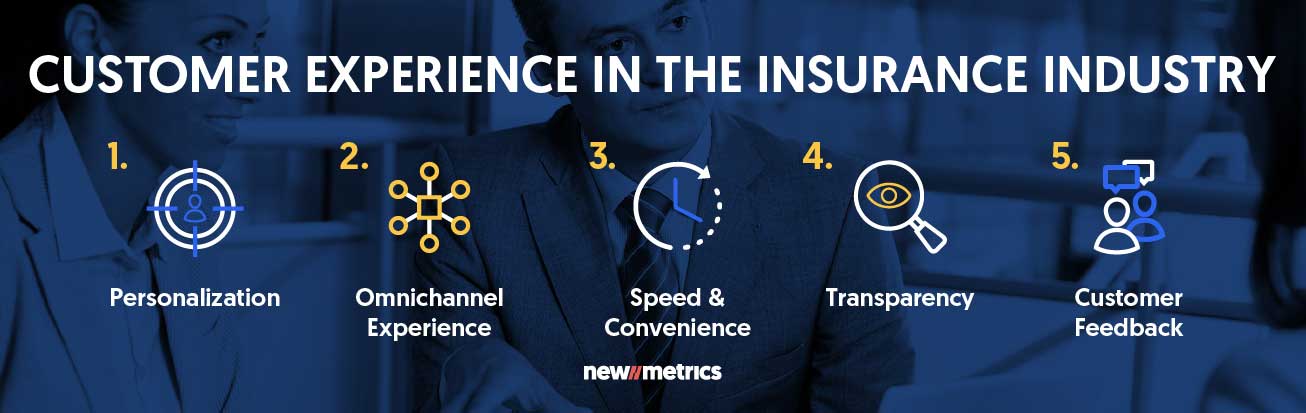

Customer Experience in the Insurance Industry

Customer experience is a critical factor in the insurance industry. It refers to customers’ overall experience when interacting with an insurance company. A positive customer experience can lead to increased customer loyalty and retention.

Here are some ways that insurers can improve customer experience:

- Personalization: Insurers should personalize their products and services to meet each customer’s unique needs. This can be done by using data and analytics to gain insights into customer behavior and preferences. For example, insurers can use data to identify customers at risk of leaving and offer personalized discounts or other incentives to stay.

- Omnichannel experience: Insurers should provide customers with a seamless omnichannel experience. This means customers should be able to interact with the insurer through multiple channels such as phone, email, chat, and social media. Insurers should also ensure customers can easily switch between channels without repeating themselves.

- Speed and convenience: Insurers should make it easy for customers to do business with them. This means providing fast and convenient service through digital channels. For example, insurers can use chatbots to provide customers with quick answers to their questions or allow customers to file claims online.

- Transparency: Insurers should be transparent about their products and services. They should provide customers with clear information about what is covered and what is not covered by their policies. Insurers should also be transparent about their pricing and fees.

- Customer feedback: Insurers should listen to their customer’s feedback and use it to improve their products and services. This can be done by conducting surveys or soliciting feedback through social media or other channels. Insurers should also respond promptly to customer complaints and take steps to address any issues that arise.

Insurance Industry Disruptors

The insurance industry is not immune to disruptions facing other industries. Customer demands are changing, traditional operating models are under pressure, and new players are emerging.

While these disruptions will not happen overnight, many of these shifts are already starting, and first movers have a clear advantage. Insurers will benefit from clearly articulating their strategy and adjusting their operating models accordingly.

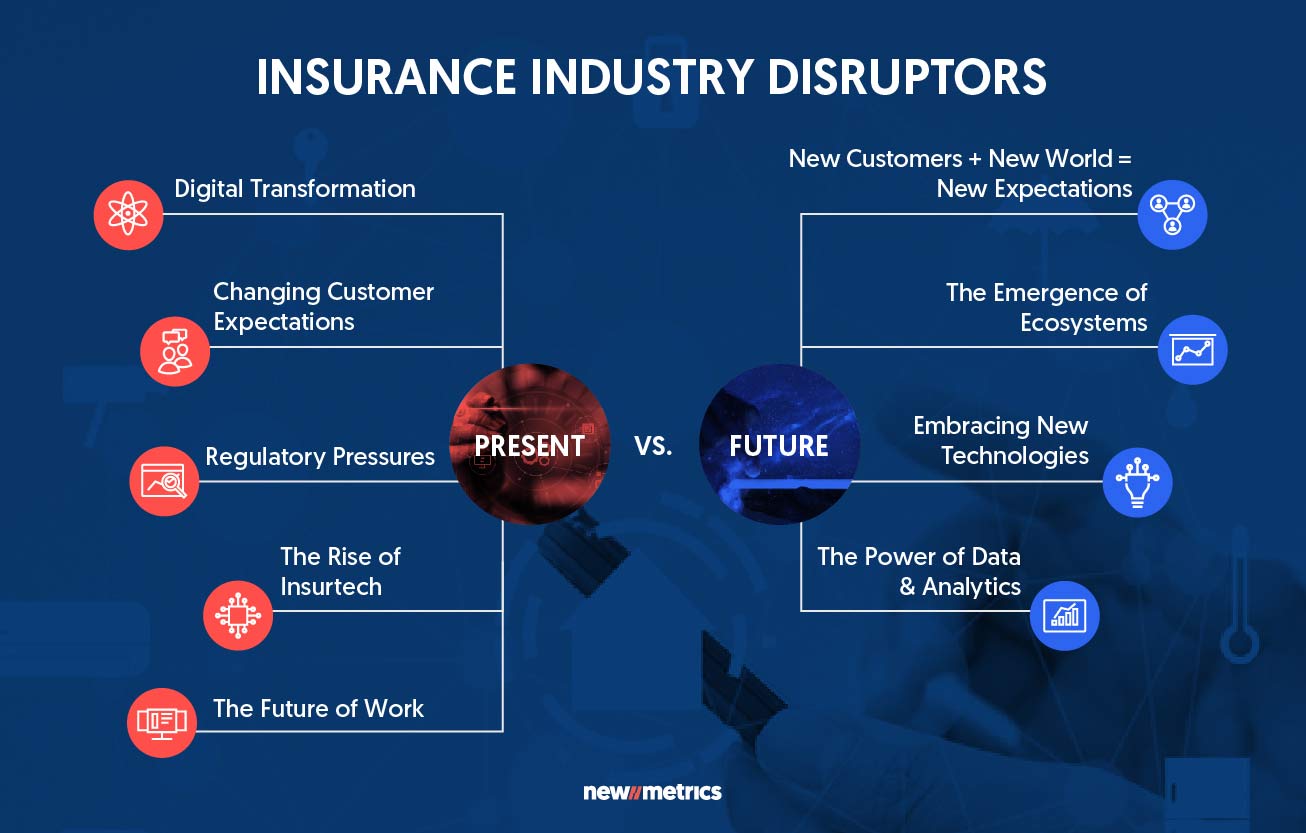

Present Day Disruptors:

The insurance industry is undergoing significant changes. These changes are needed to help insurers remain competitive in an increasingly crowded marketplace.

- Digital transformation: The rise of digital technologies is transforming the insurance industry. Insurers that need to adapt to these changes risk losing customers to competitors. Insurers should use data and analytics to gain insights into customer behavior and preferences. They should use this information to develop products and services that meet those needs.

- Changing customer expectations: Insurers demand fast, convenient, and personalized service. Insurers that fail to meet these expectations risk losing customers to competitors. Insurers should understand their customers ‘needs and preferences. They should use customer feedback to develop products and services that meet those needs.

- Regulatory pressures: The insurance industry faces increased regulatory pressures on data privacy, security, and usage. Insurers that fail to comply with these regulations risk facing significant fines and reputational damage. Here are some ways that insurers can manage these concerns:

- Data governance: Insurers should establish clear policies and procedures for managing data. This includes defining data ownership, establishing data quality standards, and ensuring compliance with regulatory requirements.

- Data security: Insurers should implement robust security measures to protect customer data from unauthorized access or theft. This includes using encryption, firewalls, and other security technologies.

- Data privacy: Insurers should be transparent about collecting, using, and sharing customer data. They should obtain customer consent before collecting personal information and only use it for legitimate business purposes.

- Regulatory compliance: Insurers should stay up-to-date with the latest data privacy and security regulations. They should also establish processes for monitoring compliance and reporting any violations.

- Data analytics: Insurers should use data analytics to gain insights into customer behavior and preferences. However, they must ensure that they use customer data in compliance with all applicable regulations.

4. The Rise of Insurtech: Insurtech refers to using technology to disrupt and innovate the insurance industry. Insurtech startups leverage technologies such as AI, blockchain, and IoT to develop new products and services. This is why insurance industries will need to partner with Insurtech to achieve:

- Digitization: Insurtech companies are playing key roles in digitizing the insurance industry, helping insurers improve their underwriting, claims, distribution, and product development efforts.

- New business models: By partnering with Insurtech startups, insurance companies can tackle newer business models such as microinsurance and on-demand insurance.

- Productivity: Successful partnerships with Insurtech startups can lead to immense gains in productivity for insurers. For example, automating claims processing can help insurers process claims more quickly and accurately.

- Efficiency: Insurtech startups can help insurers improve their efficiency by automating various processes such as underwriting and claims processing.

- Reliability: By partnering with Insurtech startups, insurers can improve their reliability by using data analytics to make more accurate predictions about risk.

5. The Future of Work: The insurance industry faces a shortage of skilled workers as baby boomers retire. To address the talent shortage, insurers can focus on transforming their talent model by developing new skills and capabilities in-house and partnering with external organizations to access new talent pools.

Developing new skills and capabilities in-house can involve upskilling current employees through training programs and providing opportunities for career development. This can help insurers retain their existing workforce while also developing new skills that are needed to meet the demands of the industry.

Partnering with external organizations can help insurers access new talent pools and bring in fresh perspectives. This can involve partnering with universities to recruit graduates or working with startups to access new technologies and ideas.

Future Disruptors:

The insurance industry is expected to evolve by adapting to new technologies and achieving net zero. In cloud adoption, insurers should start integrating their systems and data while leveraging cloud capabilities to achieve greater customer-centricity. Focusing on micro improvements utilizing industry cloud applications specific to their business could be a great next step. The following major trends could shape and upend the insurance industry over the coming years, with profound implications for both policyholders and insurers:

- New Customers + New World = New Expectations: The rise of digital technologies has shifted customer expectations. Customers now expect insurers to provide fast, convenient, personalized service through digital channels. The industry is rapidly shifting from product-led to service-led offerings that deliver a holistic experience to customers. This means that cutting-edge technologies are quickly becoming the norm. Insurance-as-a-service is a 100% digital insurance offering that covers end-to-end requirements for simpler onboarding, claims management, and customer support. This puts immense pressure on the industry and carriers to adjust, as if those expectations are not met, customers will quickly move on. Insurers should create a culture of innovation that is shifting in mindset from risk-averse to risk-tolerant. Insurers should encourage employees to experiment with new ideas and reward those who develop innovative solutions.

- The Emergence of Ecosystems: Digital ecosystems offer traditional insurers valuable opportunities to use analytics to evolve and expand their business models. They could facilitate the evolution of existing insurance businesses by advancing risk assessments, for instance, by considering safety measures like connected-home solutions. By integrating service exchange with cross-industry ecosystem partners, insurers can shape their roles and value propositions with customers in mind. For example, they can transform from purely insuring risks to preventing them via more holistic service offerings within a network. As traditional industry borders fall away, ecosystems—and the digital platforms that often enable them—will significantly influence insurers’ future.

- The Power of Data and Analytics: The insurance industry is being transformed by data analytics, which is increasing speed, efficiency, and accuracy in every aspect of insurance companies. With advanced data and predictive analytics systems, insurers can make data-driven business decisions that help them assess risk, predict losses, and optimize their underwriting and pricing strategies. This allows companies to develop more accurate and reliable risk models, reducing the likelihood of losses and improving profitability. By analyzing customer behaviors and connecting the dots, insurers can gain insights beyond the number of life insurance policies under management and their customer ownership. Additionally, imagery and geospatial intelligence enable insurers to be proactive with their coverage and protection.

- Embracing New Technologies: Insurers will need to embrace new technologies to improve products and services, reduce costs, and increase efficiency.

- Internet of Things (IoT):

- IoT-enabled risk prevention: Sensors can be used to assess risk on a more granular level. For example, sensors in warehouses can help assess risk and price policies accordingly.

- Supplier network management: IoT can be used to manage supplier networks in fleet motor insurance for garages and in directors’ and officers’ liability insurance for lawyers.

- New products and distribution channels: IoT allows insurers to develop new products and open new distribution channels.

- Prediction, prevention, and assistance: IoT can help insurers extend their roles to include prediction, prevention, and assistance.

- Artificial Intelligence AI and Machine Learning: They can help insurers in:

- Underwriting: Improves underwriting processes by analyzing data from various sources such as social media, credit scores, and public records. This can help insurers make more accurate predictions about risk and price policies accordingly.

- Fraud detection: AI and ML can help detect fraud by analyzing large amounts of data and identifying patterns that may indicate fraudulent activity.

- Claims processing: AI and ML can help automate claims processing by analyzing data from various sources such as photos, videos, and audio recordings. This can help insurers process claims more quickly and accurately.

- Blockchain: Insurers will need to rely more on Blockchain to assist in:

- Claims processing: Blockchain can automate claims processing by verifying coverage and executing payments based on predefined conditions.

- Fraud reduction: Blockchain can reduce fraud by providing a secure and transparent way to store and share data among insurers and other parties.

- Data security: Blockchain can improve data security by providing a tamper-proof way to store and share data.

- Smart contracts: Blockchain can enable smart contracts that execute programmed actions and payments based on predefined conditions.

- Lower costs: By streamlining information transfers, blockchain can help lower costs for different types of insurance, such as health insurance.

The changes in the insurance industry are much needed to keep up with evolving customer expectations, stay competitive, effectively manage risks, and comply with changing regulations. Insurance companies need to focus more on creating an excellent customer experience while managing present and future disruptors or risks becoming obsolete.